Why You Need To Name a Life Insurance Beneficiary (And How To Do It)

Written & Edited by Dan Marticio Written & Edited by Dan Marticio Dan MarticioDan Marticio is the content manager at SmartFinancial and has written 150+ articles across multiple insurance verticals.... Read more |

Editorial Standards

Editorial Standards SmartFinancial Offers Unbiased, Fact-based Information. Our fact-checked articles are intended to educate insurance shoppers so they can make the right buying decisions. Learn More

A life insurance beneficiary is an individual or entity that receives the death benefit from a life insurance policy after the insured dies. Policies may have multiple beneficiaries, which commonly include spouses, children or charity organizations.

Designating a beneficiary is essential for ensuring the right people receive the death benefit and avoiding taxation. Keep reading to learn more about how beneficiaries work.

|

Key Takeaways

|

What Is a Beneficiary in Life Insurance?

A beneficiary for life insurance is the person or entity designated to receive the death benefit upon the insured's death. The insured can name multiple beneficiaries, also called co-beneficiaries, and allocate specific percentages of the benefit to each. For example, you can designate both of your children as co-beneficiaries, with each child receiving half of the proceeds.

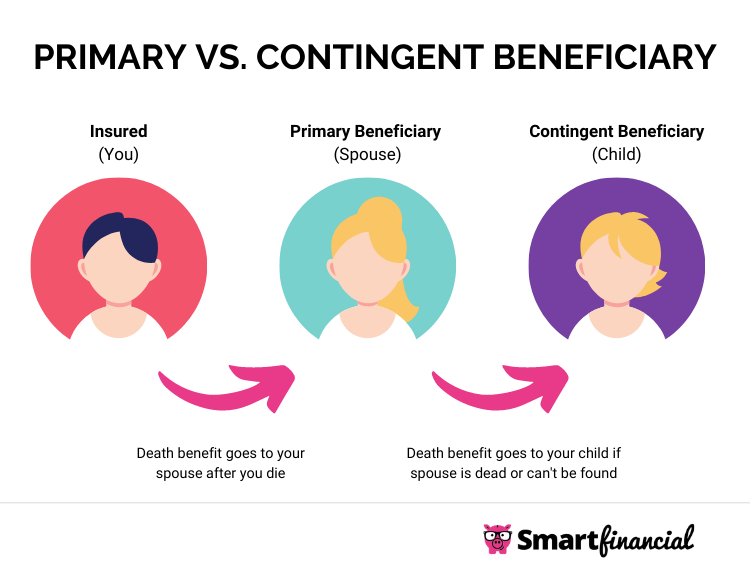

The insured can also specify primary and contingent beneficiaries. Primary beneficiaries receive the payout first, while contingent beneficiaries only receive it if the primary beneficiaries cannot. For example, you might name your spouse as the primary beneficiary and your child as the contingent beneficiary, ensuring that your child receives the benefit if your spouse cannot.

Why Do I Need To Name a Beneficiary?

There are two primary reasons why you want to designate a beneficiary. The first reason is so that the death benefit goes directly to the person or entity you want to receive it. The second reason is so that your beneficiary enjoys a tax-free claim payout, meaning that the income they receive from the life insurance settlement will not be taxable.[1]

What Happens if I Don’t Name a Beneficiary?

If you do not designate a beneficiary, the death benefit will typically go to your estate. Your estate is all the property you leave behind, which is then distributed according to your will and often facilitated by a probate court. The probate process, which can span several months, may use your assets to settle debts before distributing them to your next of kin.[2] In addition, when your death benefits go to your estate, it may be subject to taxation.[3]

Some life insurance policies will already have life insurance beneficiary rules for paying out death benefits if there is no designated beneficiary. Death benefits issued by the Office of Personnel Management (OPM), for example, will be paid out in the following order:[4]

- Your widow or widower

- Your children in equal shares

- Your parents in equal shares

- Your appointed executor or administrator of your estate

- Your next of kin under the laws of the state you live in when you die

Can I Name Anybody as a Beneficiary?

Generally, you can name anyone as a beneficiary, including family members, friends, trusts, charities or organizations. However, keep in mind that In most cases, a minor will not be able to claim a death benefit before they reach age 18 or 21. Instead, the probate court may name a custodian to manage the funds until they are of age and that appointed custodian may not always be one you would want.[5]

Who Should I Choose as My Life Insurance Beneficiary?

A life insurance beneficiary is often a family member, such as a spouse or child. You may also donate your life insurance proceeds to a charitable organization, which may carry certain tax advantages. Below are common types of beneficiaries:

- Spouse or domestic partner

- Child

- Trustee

- Charity

- Your estate

How Do I Name a Beneficiary?

When buying a life insurance policy, choosing a life insurance beneficiary is generally part of the process. The insurer typically requests the below details to ensure that your death benefits go to the correct recipient:

- Full name

- Maiden or former names

- Social security number

- Date of birth

- Nationality and passport number (for non-U.S. citizens)

In addition, your life insurance company may request you designate your beneficiaries as revocable or irrevocable when buying the policy:[6]

- Revocable beneficiary: You can change this type of beneficiary without notifying them and getting written permission.

- Irrevocable beneficiary: You must obtain written permission from this beneficiary to remove them from the policy before you can make changes.

Can You Change Beneficiaries?

Updating your beneficiary is generally a straightforward task and your insurance company will walk you through the process. When changing a beneficiary, you will typically need to submit the proper paperwork and supply the new beneficiary's full name, social security number, date of birth and other identifying information — similar to designating a beneficiary the first time around.

When Should I Update My Beneficiary?

Common life events that may result in changing your beneficiary may include:

- Getting divorced

- Getting married

- Having children

- Paying your home mortgage early

- When a family member or dependent dies

- Parents become financially dependent on you

- Your children become financially independent

Failing to update your beneficiary can create trouble after you die. For example, say you married and listed your spouse as a life beneficiary but you later divorce and remarried. You may want to remove your ex-spouse and designate your current spouse as the primary beneficiary. Otherwise, your ex-spouse will likely be legally entitled to the death benefit after you die.

Individuals can search their state database to see if they are entitled to an unclaimed life insurance death benefit. NAUPA receives tens of millions of inquiries annually and has returned more than $5 billion to the rightful owners of unclaimed property, including death benefits, refunds, annuities and more.[7]

How Can My Beneficiary Claim the Death Benefit?

After you die, the primary beneficiaries will need to obtain a certified copy of your death certificate and file a claim with the life insurance company. After confirming your death, the insurance company will walk your beneficiary through the process of claiming the death benefit.

If there are multiple beneficiaries entitled to the death benefit, then each beneficiary will need to submit a claim.[8] If a secondary beneficiary is claiming the death benefit because the primary beneficiary died, they will need to supply the death certificate of both the insured and the primary beneficiary.

If you are a primary beneficiary and want to ensure a timely death benefit payout, don't wait for the insurance company to contact you. It may be several months before the life insurance company realizes the insured has died and then contacts you.

There are several ways you can receive the death benefit and it may already be decided in advance by the insured. Generally, the death benefit payout will come in three forms:

- Lump sum payment: You receive your share of the death benefit in a single payment.

- Annuity: Your payout is converted into regular payments over time, allowing the remaining death benefit to earn interest. The insurer distributes these payments for a set period or until you die, with longer timeframes potentially increasing the total payout due to earned interest.

- Installment payments: The death benefit payout is issued in a series of payments over time — similar to a bi-monthly or monthly paycheck from a job.

Not sure if you're a beneficiary? Try searching the Life Insurance Policy Locator Service by the National Association of Insurance Commissioners. This free service may confirm your beneficiary status if the policy is with a participating company.

- Insurance quotes /

- Life /

- Life Insurance Beneficiary

Dan Marticio is the content manager at SmartFinancial and has written 150+ articles across multiple insurance verticals. His past experience writing in small business and personal finance verticals has earned him bylines on prominent fintech brands, including LendingTree, ValuePenguin, Fundera, The Balance and NerdWallet. His guides always aim to assist everyday consumers and entrepreneurs make informed decisions about their finances and business.

Get a Free Life Insurance Quote Online Now.

More on Life Insurance

Looking for Life Insurance?

Compare rates from dozens of companies in less than 3 minutes.