How Do I Save Money On Car Insurance?

Written by Dylan Tate Written by Dylan Tate Dylan TateDylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under... Read more |  Edited by Dan Marticio Edited by Dan MarticioDan MarticioDan Marticio is the content manager at SmartFinancial and has written 150+ articles across multiple insurance verticals.... Read more |

Editorial Standards

Editorial Standards SmartFinancial Offers Unbiased, Fact-based Information. Our fact-checked articles are intended to educate insurance shoppers so they can make the right buying decisions. Learn More

There are several ways you can save money on car insurance, from adjusting your driving habits to hunting for discounts at different insurance companies. Since car insurance is required by law in almost every state, it is important to find a policy that provides the best value for your specific circumstances and your budget.

Keep reading for 13 tips that can help you know how to save money on car insurance.

|

Key Takeaways

|

On This Page

1. Shop Around

2. Make Sure Your Information Is Updated and Accurate

3. Ask Insurance Carriers About Discounts

4. Drop Coverage You Don’t Need

5. Work on Your Credit Score

6. Increase Your Car Insurance Deductibles

7. Review Your Policy Annually

8. Bundle Policies

9. Consider Multi-Vehicle Discounts

10. Opt for Low-Mileage or Usage-Based Insurance

11. Select Car Models With Cheap Insurance Rates

12. Keep Your Car Stored in a Safe Area

13. Complete a Defensive Driving Course

FAQs

1. Shop Around

Shopping around can help you find the best car insurance rate because many insurers will offer different rates for the exact same amount of coverage. Every insurance company uses its own formula to calculate the risk of insuring any given person and can weigh certain factors differently than others.

As a result, it’s important to comparison shop to find the insurance company that can provide the most favorable rate for you. For example, one insurance company could offer the cheapest insurance for safe drivers, but a different company may have the lowest rates for high-risk drivers.

You can use an insurance marketplace like SmartFinancial to discover the insurance policy that best suits your situation without going through the trouble of contacting multiple insurance companies individually.

2. Make Sure Your Information Is Updated and Accurate

Giving your insurance provider up-to-date information about your driving habits can also help save you money on car insurance. For example, if you previously had to commute to work, you should let your insurance company know if you accept a remote job. Driving less means you’re less likely to get into an accident and your insurer may lower your rate as a result.

It’s important to provide your insurer with accurate information about the negative things too. For example, failing to inform your insurer about an accident may be considered fraud. If you are caught withholding information or lying to your insurance company, your policy could be canceled and you could experience a lapse in coverage. This could result in you paying more for car insurance when you reactivate your policy.

3. Ask Insurance Carriers About Discounts

An insurance company may offer you a discounted rate for several reasons. For example, Allstate offers a safe driving bonus that contributes toward your car insurance payment anytime you go six months without getting into a car accident.[1] Meanwhile, many insurers offer discounted rates for good students who have a GPA of 3.0 or higher.

In addition, your insurance company is required to offer you a discount for installing an anti-theft device if you live in one of the following states:[2]

- Florida

- Illinois

- Kentucky

- Louisiana

- Massachusetts

- Minnesota

- New Mexico

- New York

- Pennsylvania

- Rhode Island

- Texas

- Washington

4. Drop Coverage You Don’t Need

You may be able to save money on your car insurance by dropping optional coverage types. While your lender will likely require you to have comprehensive and collision coverage if you are paying off your car, you are free to remove them from your policy once you have finished paying off your car.

When deciding whether to keep these coverage types, you should consider whether the potential payout after a total loss is worth the cost of your regular payments. If the cost of maintaining comprehensive and collision coverage is more than 10 times the value of your car, it may be time to drop them.[3]

5. Work on Your Credit Score

In most states, improving your credit score could help you save on car insurance. Some companies will calculate your premium using a credit-based insurance score. As a result, fully paying off your credit card debt each month and consistently making mortgage payments on time could lead to lower car insurance premiums.

However, the use of credit-based insurance scores is restricted in a few states. If you live in California, Hawaii, Maryland or Massachusetts, you likely don’t have to worry about your credit history impacting the cost of your car insurance.[4]

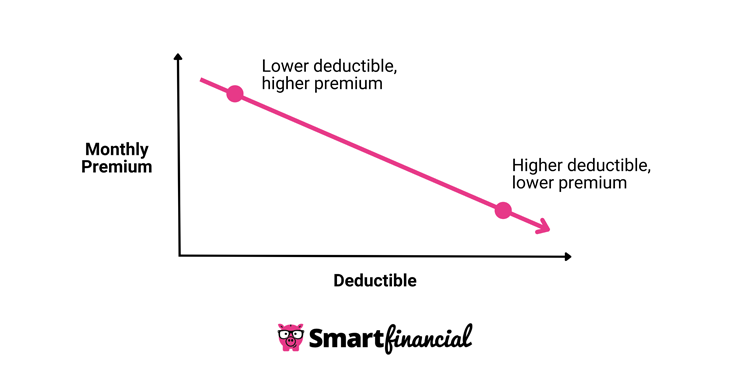

6. Increase Your Car Insurance Deductibles

Your car insurance premium will go down if you raise your deductible because your insurance company will be responsible for paying less whenever you make a claim. Your deductible is the minimum amount you agree to pay toward a covered loss before your insurance company will start chipping in.

For example, if you have a $500 deductible for collision coverage and you cause $2,000 worth of damage to someone else’s car in an accident, then your insurance company would pay $1,500. While liability insurance does not have a deductible, coverage types like comprehensive and collision coverage do. As a result, you could save money on your premiums if you can afford to pay more money upfront anytime you need to file an insurance claim.

7. Review Your Policy Annually

You should review your policy annually to see if there are opportunities for your car insurance to go down. In general, cars become cheaper to insure over time as they age and become less valuable. You can use an online resource like Kelley Blue Book to estimate the value of your car and determine if you should be paying less for auto insurance.

8. Bundle Policies

Many insurance companies offer discounted rates if you purchase multiple insurance products from them. For example, bundling your home, auto and life insurance policies may result in you paying less than if you purchased all of them individually.

9. Consider Multi-Vehicle Discounts

Insurance companies usually offer discounts if you insure multiple vehicles under one policy. This can apply if you add all of your immediate family members’ cars to one policy or if you simply add a second vehicle that you personally drive. All the cars on a multi-vehicle policy generally have to be kept at the same address, although your insurer will likely still cover your child’s car even if they are away at college.

10. Opt for Low-Mileage or Usage-Based Insurance

If you drive your car infrequently, you may be eligible for usage-based car insurance, also known as black box insurance or telematics insurance. When you sign up for a usage-based insurance policy, you will have to attach a device to your car or download a mobile app that records your driving data like how often you drive and how long your typical commutes are. Your insurer will then use that data to either adjust your premium directly or calculate your discount amount.

For example, Nationwide’s SmartMiles program charges drivers a base rate that stays consistent from month to month and a variable rate that changes based on the number of miles they drove over the past month.[5] To improve your odds of qualifying for low-mileage insurance, you could consider carpooling to work or using public transportation more frequently.

11. Select Car Models With Cheap Insurance Rates

The age and model of your car have a significant impact on the cost of your auto insurance. Newer cars may earn you a discounted rate if they have built-in safety features. At the same time, a car with high-end technology is more expensive to repair, so it’s more likely that your insurance company will declare it a total loss after an accident. For this reason, newer cars can be a greater risk to insure and may carry higher premiums as a result.

Conversely, older cars are generally cheaper to insure since the cost of reimbursing you after a total loss is much lower for your insurance company. If you need a car and want to get the cheapest insurance possible, it might be better to buy a used car than a brand new one. In addition, if you can afford to pay for the vehicle upfront, you may be able to forego comprehensive and collision coverage, allowing you to save even more money on insurance.

12. Keep Your Car Stored in a Safe Area

Parking your car where it is unlikely to be stolen or broken into can save you money on comprehensive coverage since it decreases the odds that you will have to make a theft or vandalism claim. While you may not be able to easily change where you live, investing in a locked garage to park your cars in may lower the cost of your auto insurance premiums.

13. Complete a Defensive Driving Course

Some insurance companies will offer you a discount on your car insurance premium if you complete a defensive driving course. Even without considering potential discounts, a defensive driving course could teach you techniques for preventing costly accidents and help you avoid filing an insurance claim that would raise your rates.

The availability of defensive driving discounts typically depends on the state you live in and, in many cases, your age. For example, Farmers only offers defensive driving discounts for people over the age of 55 or 65, depending on the state.[6]

- Insurance quotes /

- Auto /

- How To Save Money Auto Insurance Policy

Dylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under his belt. He has over seven years of experience writing for online publications, primarily about gaming and esports. In the process, he has become an expert in search engine optimization, news reporting, feature writing and copy editing.

Get a Free Auto Insurance Quote Online Now.

More on Auto Insurance

Looking for Auto Insurance?

Compare rates from dozens of companies in less than 3 minutes.