Hurricane Milton: Current Impact and Costs for Consumers and Insurance Companies

Written by Dylan Tate Written by Dylan Tate Dylan TateDylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under... Read more |  Edited by Dan Marticio Edited by Dan MarticioDan MarticioDan Marticio is the content manager at SmartFinancial and has written 150+ articles across multiple insurance verticals.... Read more |

Editorial Standards

Editorial Standards SmartFinancial Offers Unbiased, Fact-based Information. Our fact-checked articles are intended to educate insurance shoppers so they can make the right buying decisions. Learn More

Hurricane Milton became one of the costliest natural disasters in American history when it hit the state of Florida in October 2024. Along with killing multiple people, the hurricane caused billions of dollars worth of losses for insurance companies and set the stage for slower economic growth in multiple sectors.

Keep reading to learn more about Hurricane Milton’s impact on Florida and what programs may be available to you if your home is affected by a natural disaster like a hurricane.

|

Key Takeaways

|

On This Page

What Is Hurricane Milton?

Hurricane Milton’s Impact on Consumers

Insurance Coverage for Hurricane Milton

Will Insurance Premiums Increase After Hurricane Milton?

What Types of Government and Disaster Assistance Programs Are There?

How To Prepare for a Natural Disaster Like Hurricane Milton

FAQs

What Is Hurricane Milton?

Hurricane Milton was a tropical cyclone that struck the United States on October 9 and October 10, 2024, predominantly affecting the state of Florida. Milton originated as a tropical depression that formed in the Gulf of Mexico on October 5, according to the National Hurricane Center. The storm rapidly intensified, with its wind speeds increasing by at least 130 miles per hour within the span of around 48 hours.[1]

At its peak, Milton was a Category 5 cyclone and the strongest hurricane in the Gulf of Mexico since Hurricane Rita in 2005.[1] It eventually made landfall as a Category 3 hurricane near Siesta Key on Florida’s Gulf Coast, and then Hurricane Milton passed through Central Florida and weakened to Category 1 before moving past the state’s east coast and into the Atlantic Ocean.[2] Hurricane Milton resulted in the deaths of at least two dozen people, many of whom were killed by hurricane-induced tornadoes that hit cities like Fort Myers.[3][4]

Hurricane Milton’s Impact on Consumers

See the following sections for an overview of Hurricane Milton’s impact on consumers, including the extent of the property damage and other financial setbacks it caused.

Property Damage

Counting losses covered by insurance alone, Hurricane Milton caused an estimated $30 to $50 billion worth of property damage, making it one of the most expensive natural disasters to ever hit the United States. The high rebuilding costs in Florida are likely to be exacerbated by the fact that Milton came only two weeks after Helene ravaged western North Carolina and other Southeastern states, meaning the demand for materials and labor is much higher relative to the supply than normal.[2]

Fortunately, the areas that were devastated by Hurricane Helene weeks earlier generally did not take a direct hit from Hurricane Milton. Additionally, it’s worth noting that Milton is now estimated to be only about half as costly as the $60 to $100 billion figure that was initially projected.[5]

Nevertheless, Hurricane Milton had a very tangible effect across Florida, as numerous homes were destroyed, streets were overrun with mud and millions of people lost power. Other notable examples of property damage caused by Milton include the roof of a baseball stadium being torn off and a giant crane falling and crashing into a building.[4]

Financial Costs

Along with costs related to repairing or replacing property, there will likely be broader economic repercussions in the wake of Hurricane Milton. Florida’s gross state product (GSP) growth is projected to drop by 3 to 4 percentage points in Q4 due to the storm, accounting for a drop in the country’s overall gross domestic product (GDP) growth by 0.2 to 0.4 percentage points. Industries expected to take a major hit include tourism, construction, retail and energy.[6]

In addition, insurance prices will likely be impacted by Hurricane Milton, particularly due to the Florida insurance market’s heavy reliance on reinsurance. While reinsurance prices for property insurers in Florida dropped by as much as 10% in the summer of 2024, it’s unlikely that prices will drop again in 2025 because of the damage from the storm.[2]

The good news is that property reinsurance prices are high enough now that they shouldn’t have to increase dramatically in 2025 as they did in 2023. Even so, Floridian homeowners insurance and auto insurance policyholders can likely expect level-to-rising premiums going into next year as insurance carriers pass their reinsurance costs on to their customers.[2]

Insurance Coverage for Hurricane Milton

Insurance coverage for hurricanes like Milton is generally secured through a combination of home and flood insurance. A standard homeowners policy should insure your house and items against damage from wind and falling objects, along with theft that occurs after you evacuate the premises amid a hurricane. That said, you may need additional wind and hail coverage if you live in a region that is particularly prone to windstorms, such as the Texas Gulf Coast.[7]

Meanwhile, flooding and storm surge damage are excluded from standard home insurance coverage, meaning you will need additional coverage to account for flood damage caused by a hurricane, regardless of where you live. The majority of flood insurance policyholders are insured through the federal government’s National Flood Insurance Program (NFIP), though you may also be able to obtain coverage from a private insurance company that underwrites its own policies.[8]

Will Insurance Premiums Increase After Hurricane Milton?

Your insurance premiums will likely go up if you file a claim for hurricane-related damage. Even if your property has been spared from significant damage and you don’t personally need to file a claim, you could still encounter higher rates if your area has incurred a large amount of damage due to Hurricane Milton, since insurance companies may need to raise premiums across the board to offset their losses amid an increase in Hurricane Milton insurance claims in the area.

What Types of Government and Disaster Assistance Programs Are There?

The next few sections will overview some of the main public and private programs that exist to support individuals living in regions impacted by natural disasters.

FEMA

The Federal Emergency Management Agency (FEMA) is the United States government’s primary institution for providing relief after a natural disaster. If your region has been declared as a disaster area by the federal government, you can apply for up to $770 from FEMA to cover your immediate needs, and you may also qualify for additional assistance related to expenses like temporary housing and basic home repairs.[9]

FEMA also administers the NFIP. Although the average FEMA disaster assistance grant from 2016 to 2022 was $3,000, the average NFIP flood insurance claim payout was over $66,000 during that same time frame.[10] You should note that, if you live in a high-risk flood zone and receive disaster assistance from a federal agency like FEMA, you can’t qualify for further aid unless you purchase flood insurance.[11]

D-SNAP

The Disaster Supplemental Nutrition Assistance Program (D-SNAP), also known as disaster food stamps, provides people living in presidentially declared disaster areas with funds loaded onto an electronic benefits transfer (EBT) card so they can pay for food in the aftermath of a natural disaster. You may qualify if you are experiencing evacuation or relocation costs, a loss of income, an injury or other burdensome expenses because of a disaster.[12]

Disaster Loans and Mortgage Assistance

Low-interest loans are available for individuals and businesses in federal disaster areas through the Small Business Administration (SBA). There are various types of SBA disaster loans that can be used for different purposes, such as repairing or replacing damaged or destroyed property, covering losses that aren’t covered by your homeowners or commercial insurance or taking care of other personal expenses.[13]

Meanwhile, homeowners with mortgages backed by the Federal Housing Administration (FHA) can qualify for help in making mortgage payments after a natural disaster. Additionally, if you need to purchase a new home because of the disaster, you can take out a mortgage through the FHA that requires no down payment. Keep in mind that this type of loan will require mortgage insurance, the cost of which will be included in your monthly mortgage payments.[14]

Unemployment Benefits

The government also offers short-term unemployment benefits to workers in federally declared disaster areas who have lost their jobs, cannot work due to an injury or are physically unable to get to work because of a natural disaster. Be aware that unemployment benefits are distributed at the state level rather than the federal level.[15]

Private Organizations

In addition to the assistance provided by the federal government, there is often support available from a large number of nonprofits and other private organizations that mobilize following natural disasters. Examples of charities that have participated in recovery efforts in the aftermath of Hurricane Milton include Convoy of Hope, the American Red Cross and the International Medical Corps.

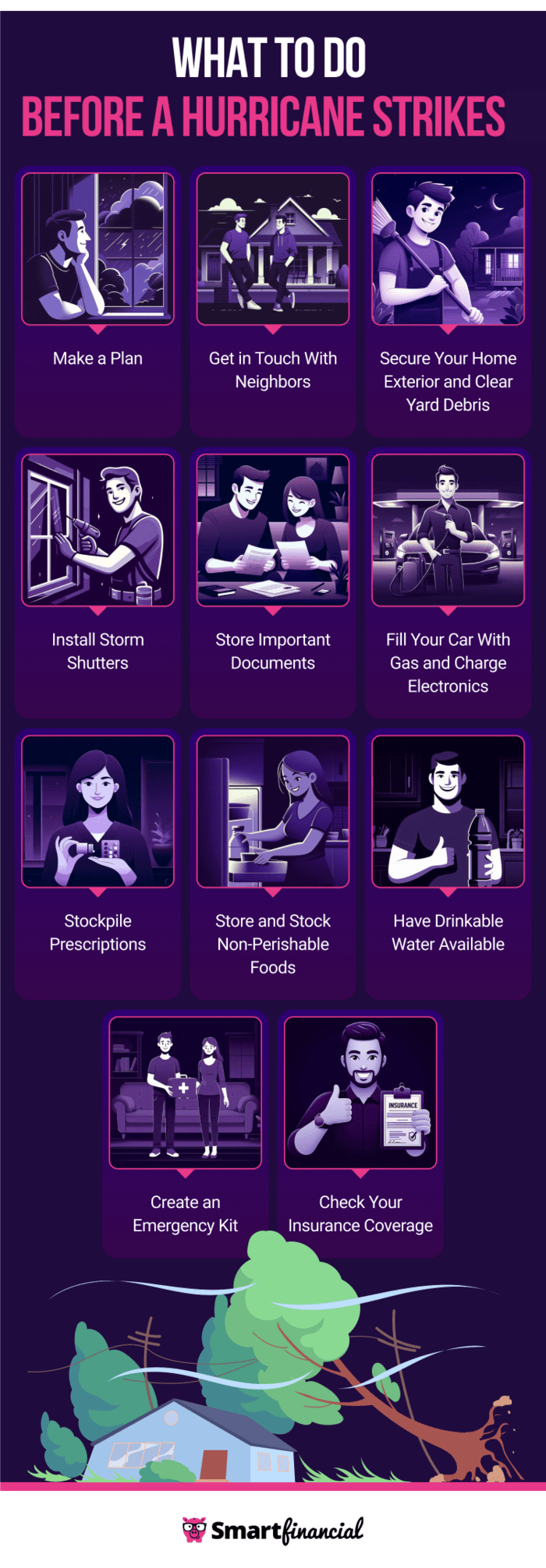

How To Prepare for a Natural Disaster Like Hurricane Milton

In general, you should take the following steps to prepare for a hurricane or a similar natural disaster:

- Decide whether you intend to evacuate the area or stay at home after the National Hurricane Center issues a tropical storm warning for your region.

- Contact your neighbors to inform them about your decision.

- Tie down loose objects, including outdoor furniture, and clean up debris outside of your home.

- Have storm shutters installed on your windows.

- Make sure all of your important documents are stored in a safe place where they are unlikely to be destroyed by high winds or floodwaters.

- Fully charge all of your electronics and fill your cars with gasoline.

- Refill your prescriptions early to make sure you have an ample supply.

- Buy nonperishable foods and store them in waterproof containers.

- Stock up on drinking water.

- Assemble an emergency kit that includes items like flashlights, blankets, cash and first aid items.

- Take a look at your home insurance policy to make sure you understand what your deductible is and what types of damage your insurer will cover.

- Insurance quotes /

- Hurricane Milton

Dylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under his belt. He has over seven years of experience writing for online publications, primarily about gaming and esports. In the process, he has become an expert in search engine optimization, news reporting, feature writing and copy editing.

Get a Free Insurance Quote Online Now.

More on Insurance

Get a Free Insurance Quote.

Compare rates from dozens of companies in less than 3 minutes.