How Does FEMA Work With My Homeowners Insurance?

Written by Dylan Tate Written by Dylan Tate Dylan TateDylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under... Read more |  Edited by Dan Marticio Edited by Dan MarticioDan MarticioDan Marticio is the content manager at SmartFinancial and has written 150+ articles across multiple insurance verticals.... Read more |

Editorial Standards

Editorial Standards SmartFinancial Offers Unbiased, Fact-based Information. Our fact-checked articles are intended to educate insurance shoppers so they can make the right buying decisions. Learn More

The Federal Emergency Management Agency (FEMA) can complement your homeowners insurance policy by covering damage that isn’t covered by your home insurance or exceeds the amount of money your insurance company will pay you. In general, FEMA and homeowners insurance only work together for people living in presidentially declared disaster areas.

FEMA has provided individual financial aid to those affected by Hurricane Katrina, Hurricane Floyd and other tragic disasters. Continue reading to learn more about how FEMA works with insurance and what steps need to be taken to secure insurance reimbursement or federal disaster aid for homeowners.

|

Key Takeaways

|

What Is FEMA?

FEMA is an agency of the United States government that helps state and local governments prepare for, respond to and recover from natural disasters. Jimmy Carter issued an executive order establishing FEMA as an independent agency in 1979, and it became a subset of the Department of Homeland Security in 2003.[1] From 2016 to 2022, FEMA awarded an average of $3,000 to each eligible homeowner who applied for disaster assistance.[2]

How Does FEMA Support Homeowners?

In the aftermath of a natural disaster, homeowners can apply for direct assistance through FEMA’s Individuals and Households Program (IHP). The IHP provides funds for serious needs, such as temporary living expenses, property repairs or replacements and hazard mitigation assistance. This program may also provide you with a temporary housing unit if there are no other housing resources available in your area.[3]

In addition, FEMA partners with nonfederal governments and other organizations to provide various resources for homeowners, including the following:[4]

- Sheltering, feeding, supply distribution and other emergency response activities

- Crisis counseling

- Formation of recovery plans for disaster survivors

- Legal aid for low-income disaster survivors

- Unemployment assistance

- Coordination of private voluntary organizations

What Does FEMA Cover?

FEMA provides coverage for a wide array of services after your home has been impacted by a natural disaster. See the below table for several examples of covered services:[5]

|

Reimbursement for hotel or motel stays |

Medical and dental expenses related to an injury or illness caused by the disaster |

|

Rental assistance |

Funeral expenses |

|

Home repair or replacement |

Child care |

|

Home modifications related to accessibility for disabled people |

Moving and storage costs |

|

Restoration of privately owned access routes, like roads, bridges and docks |

Assistance with the rental or purchase of items needed after a disaster, such as generators or chainsaws |

|

Temporary leasing of residential properties |

Group flood insurance |

|

Displacement assistance |

Minor repairs needed to prevent health and safety issues |

|

Repair or replacement of personal property, including items related to a home-based business |

Assistance with immediate needs like food, water, fuel and infant care products |

|

Transportation assistance |

Will FEMA Cover Everything My Homeowners Insurance Doesn’t?

FEMA generally doesn’t cover food that goes bad due to a power outage or items that are considered to be nonessential, such as dishwashers and home theaters.[6] Nevertheless, FEMA can cover a wide range of otherwise uninsured or underinsured losses, including damage from perils that aren’t covered by your home insurance, like flooding; damage to uninsured structures, like wells or septic systems; and losses that exceed the coverage limits of your insurance policies.[7]

Keep in mind that FEMA will not overlap with your insurance, so you will generally need to submit documentation showing your insurance payout or proof that your policy doesn’t cover a certain loss before FEMA will reimburse you. Additionally, FEMA will award no more than $42,500 for each of Housing Assistance and Other Needs Assistance to any one homeowner during the 2024 fiscal year.[7]

What’s the Difference Between FEMA and Homeowners Insurance?

While FEMA is a governmental organization that provides support exclusively for people who have been impacted by expensive natural disasters, homeowners insurance is a product offered by private companies that provides coverage in case any covered peril causes sudden and unexpected damage to your property.

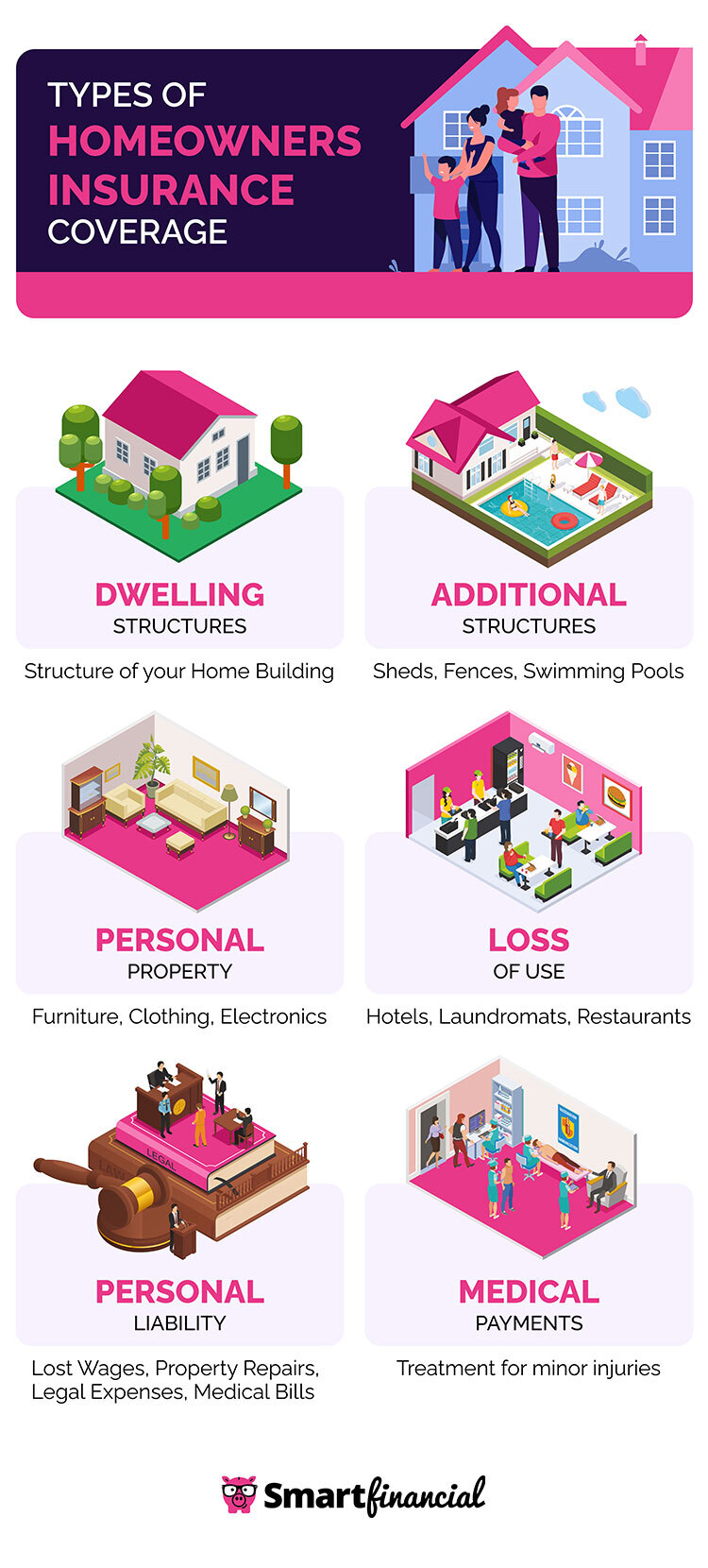

A standard home insurance policy includes dwelling coverage, which insures the structure of your home against all perils that aren’t specifically named as exclusions in the policy, and personal property coverage, which insures your belongings against the perils listed in the table below.

|

Volcanic eruptions |

|

|

Explosion |

Falling objects |

|

Riot or civil commotion |

Weight of ice, sleet or snow |

|

Damage by aircraft |

Water/steam discharge from home systems and appliances |

|

Damage by vehicle |

Sudden/accidental tearing, cracking, burning or bulging of home systems |

|

Smoke |

Freezing of home systems |

|

Vandalism or malicious mischief |

Sudden/accidental power surges |

Homeowners insurance also includes other structures coverage for structures on your property that aren’t attached to your home, loss of use coverage for additional living expenses that arise when a covered peril renders your home uninhabitable, personal liability coverage to protect you from bodily injury and property damage lawsuits and medical payments coverage to take care of minor injuries a guest incurs on your property.

When Can You Apply for FEMA Assistance?

You can only apply for assistance from FEMA if you live in a place that has been designated as a disaster area by the president of the United States. Keep in mind that this is not the same as living in a state where the governor has declared a state of emergency. You can check whether your area is a federally declared FEMA region and see the deadline by which you must apply for aid at DisasterAssistance.gov.[8]

To verify your eligibility for FEMA aid, you may need to share your Social Security number and citizenship or immigration status when you apply. Depending on the type of aid you are applying for, you may also need to prove that you own and/or primarily reside in the house that needs to be repaired or replaced.[9]

Do I Need To Purchase Flood Insurance if I Can Apply for FEMA Aid?

You can apply for and receive a grant from FEMA at least once without having to purchase flood insurance. However, if you live in a high-risk flood zone, you cannot receive federal disaster aid through FEMA or the Small Business Administration multiple times unless you obtain a flood insurance policy.[10]

Is Filing a Claim With FEMA the Same as Filing a Homeowners Insurance Claim?

FEMA is completely unrelated to your home insurance company, which means that applying for federal assistance through FEMA will not raise your insurance premiums like filing insurance claims on your homeowners policy would.

As a result, you should not expect to circumvent your insurance carrier and apply for free assistance from FEMA without having to pay a deductible or experience an increase in your insurance rates. Instead, you should view FEMA disaster aid as a way to supplement your insurance coverage rather than replace it altogether.

How To File a Claim With Homeowners Insurance and FEMA

You can take the following steps to file a homeowners insurance claim after a natural disaster:

- Dial 911 if your claim is related to a crime like theft so the responding officers can complete a police report.

- Contact your homeowners insurance provider to inform it about the damage and set up an appointment with an insurance adjuster.

- Take pictures and film videos of the damage, and reach out to a contractor in the area who can give you an idea of how much it will cost to repair the damaged property.

- Conduct emergency repairs as needed to keep your property from experiencing additional, unnecessary damage.

- Let your mortgage lender know that you have an insurance claim in progress.

- Present photos and videos, police reports, repair estimates, home inventories and other evidence that supports your claim to the insurance adjuster.

- Keep track of receipts, invoices and other documents that are relevant to your claim.

- Pay attention to the status of your claim so you can take care of any issues that arise and fill out paperwork in a timely manner.

- Use the insurance settlement to complete repairs or, if the payout is too low, get in touch with a public adjuster or lawyer to help you dispute the insurance company’s offer.

Meanwhile, you can fill out an application for FEMA aid online by using the FEMA app or DisasterAssistance.gov, over the phone by calling 1-800-621-3362 or in person by visiting a Disaster Recovery Center. Make sure you have the following information at the ready when you apply:[11]

- Social Security number

- Insurance information

- Summary of the damage

- Annual household income

- Contact information

- Banking information for direct deposit

- Insurance quotes /

- Home /

- Fema And Home Insurance

Dylan Tate is an insurance content expert for SmartFinancial with 70+ articles about home, auto and life insurance under his belt. He has over seven years of experience writing for online publications, primarily about gaming and esports. In the process, he has become an expert in search engine optimization, news reporting, feature writing and copy editing.

Get a Free Home Insurance Quote Online Now.

More on Home Insurance

Looking for Home Insurance?

Compare rates from dozens of companies in less than 3 minutes.